[Market Eye] Kospi’s rebound to 3,000 unlikely to happen anytime soon

Analysts cite high inflation, fears of recession and Russia-Ukraine war as negative factors that would continue to weigh on the Kospi in H2

Published : 2022-06-29 14:32:25

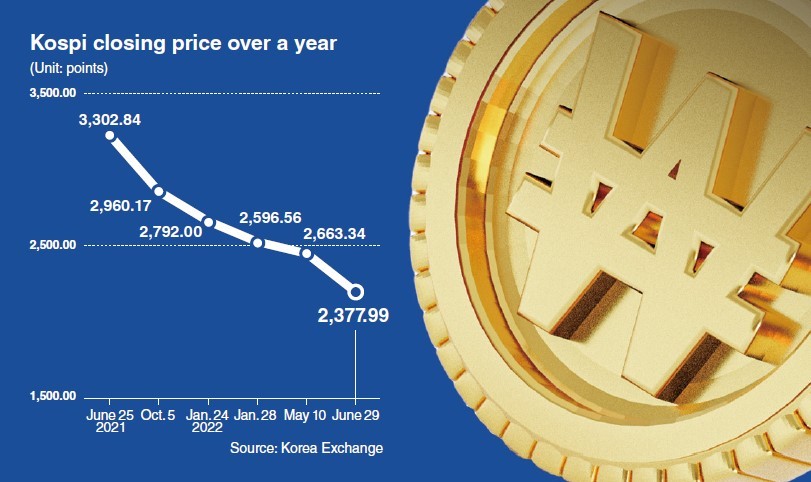

When South Korea’s key stock index surpassed the 3,000-mark for the first time in its 40-year history in January 2021, it seemed the bull market would last forever. But risks stemming from high inflation, fears of recession and the global supply bottleneck this year has beaten down the index down to some 2,400 points as of this week, with analysts warning investors that they are unlikely to feel the relief of recovering to 3,000 anytime soon.

“Our base Kospi target of 3,000 implies the MSCI KR target forward price/earnings ratio of 10x and 20 percent year-over-year earnings per share growth in estimated 2023,” JJ Park, JP Morgan’s Head of Korea Equity Research told The Korea Herald on Tuesday. A P/E of 10x means a company is trading at a multiple that is equal to 10 times earnings.

“Given a downside risk to the 2023 financial year earnings estimation amid macro headwinds including prolonged inflationary pressure, however, rebounding to 3,000 may not materialize in the near-term,” he added.

The US Federal Reserve’s decision to deliver its biggest rate hike since 1994 of 0.75 percentage point to combat high inflation has rattled the Korean equity market, affecting borrowing rates, the won-dollar exchange rate and investor sentiment. Foreigners offloaded a net 18.9 trillion won ($14.6 billion) worth of Korean equities so far this year, with some 28 percent of the total or 5.3 trillion won having sold this month.

“There is a lot of uncertainty still from US inflation and growth outlook, ongoing conflict in Eastern Europe and China‘s dynamic zero-COVID strategy,” Chetan Seth, Regional Asia Pacific Equity Strategist at Nomura said via e-mail.

“Thus, Nomura sees a wide range for Kospi over the next 12 months where the index is likely to be in the range of 2,480-3,100.”

Nomura recently lowered its investment rating on the Korean market from “overweight” to “neutral,” while global other investment banks such as Goldman Sachs and Macquarie Securities, each slashed Kospi’s top-end target from 3,350 to 3,050 and 3,200 to 2,800, respectively, early last month.

Meanwhile, local brokerages have readjusted their forecast for Kospi this week, painting a bleaker picture compared with those of global IBs.

KB Securities, the brokerage unit under the nation’s No.1 banking group by total assets, now projects a target range of 2,100 to 2,750 for the second half of the year. Samsung Securities and Hana Financial Investment each forecast a range of 2,200 to 2,700 and 2,350 to 2,650 for the same period, respectively.

“The risk of contraction in consensus earnings growth estimates for Kospi -- which if materializes due to fears of recession -- will likely continue to weigh on Korea’s benchmark index,” Seth said.

Seth however, brushed off growing concerns of a possible market crash, saying that the Korean market has already factored in risks from the US Fed’s aggressive rate hikes.

“However, the good news is that risk of a ‘crash’ is low as Korean equity market valuations have already corrected meaningfully over the past 6-12 months as the market has priced in aggressive rate hikes by the Fed and also hikes by the Bank of Korea,” Seth added.

South Korea’s central bank, which has carried out a total of five pandemic-era rate hikes since August last year, is projected to raise it benchmark interest rate yet again next month, to keep in line with the US Fed. The BOK’s benchmark interest rate currently stands at 1.75 percent, and analysts project it to reach 3 percent by the end of the year.

For those hoping to see the Kospi rebound, they may have to wait until the situation surrounding the global supply disruptions improve and its waves reach the market, possibly next year.”

“In the second half of 2022, we expect to see gradually alleviating supply chain issues with recovery from COVID-19 (especially in China) along with better shipping situations, which could reduce inflationary pressures to some extent. However, uncertainties regarding Russia-Ukraine will likely be intact to weigh on oil prices which remains a key swing factor for overall macro economy,” Park of JP Morgan said.

“Although Kospi is currently trading at trough multiple, we expect decelerating inflation in the second half onwards to be the biggest market driver. Also, we should continue to monitor the degree of economic growth deterioration in exchange of alleviating inflation,” Park said.

Last month, South Korea’s consumer prices, a major gauge of inflation, jumped 5.4 percent on-year, the sharpest rise in almost 14 years. It accelerated from a 4.8 percent gain the previous month.

(mkjung@heraldcorp.com)

“Our base Kospi target of 3,000 implies the MSCI KR target forward price/earnings ratio of 10x and 20 percent year-over-year earnings per share growth in estimated 2023,” JJ Park, JP Morgan’s Head of Korea Equity Research told The Korea Herald on Tuesday. A P/E of 10x means a company is trading at a multiple that is equal to 10 times earnings.

“Given a downside risk to the 2023 financial year earnings estimation amid macro headwinds including prolonged inflationary pressure, however, rebounding to 3,000 may not materialize in the near-term,” he added.

The US Federal Reserve’s decision to deliver its biggest rate hike since 1994 of 0.75 percentage point to combat high inflation has rattled the Korean equity market, affecting borrowing rates, the won-dollar exchange rate and investor sentiment. Foreigners offloaded a net 18.9 trillion won ($14.6 billion) worth of Korean equities so far this year, with some 28 percent of the total or 5.3 trillion won having sold this month.

“There is a lot of uncertainty still from US inflation and growth outlook, ongoing conflict in Eastern Europe and China‘s dynamic zero-COVID strategy,” Chetan Seth, Regional Asia Pacific Equity Strategist at Nomura said via e-mail.

“Thus, Nomura sees a wide range for Kospi over the next 12 months where the index is likely to be in the range of 2,480-3,100.”

Nomura recently lowered its investment rating on the Korean market from “overweight” to “neutral,” while global other investment banks such as Goldman Sachs and Macquarie Securities, each slashed Kospi’s top-end target from 3,350 to 3,050 and 3,200 to 2,800, respectively, early last month.

Meanwhile, local brokerages have readjusted their forecast for Kospi this week, painting a bleaker picture compared with those of global IBs.

KB Securities, the brokerage unit under the nation’s No.1 banking group by total assets, now projects a target range of 2,100 to 2,750 for the second half of the year. Samsung Securities and Hana Financial Investment each forecast a range of 2,200 to 2,700 and 2,350 to 2,650 for the same period, respectively.

“The risk of contraction in consensus earnings growth estimates for Kospi -- which if materializes due to fears of recession -- will likely continue to weigh on Korea’s benchmark index,” Seth said.

Seth however, brushed off growing concerns of a possible market crash, saying that the Korean market has already factored in risks from the US Fed’s aggressive rate hikes.

“However, the good news is that risk of a ‘crash’ is low as Korean equity market valuations have already corrected meaningfully over the past 6-12 months as the market has priced in aggressive rate hikes by the Fed and also hikes by the Bank of Korea,” Seth added.

South Korea’s central bank, which has carried out a total of five pandemic-era rate hikes since August last year, is projected to raise it benchmark interest rate yet again next month, to keep in line with the US Fed. The BOK’s benchmark interest rate currently stands at 1.75 percent, and analysts project it to reach 3 percent by the end of the year.

For those hoping to see the Kospi rebound, they may have to wait until the situation surrounding the global supply disruptions improve and its waves reach the market, possibly next year.”

“In the second half of 2022, we expect to see gradually alleviating supply chain issues with recovery from COVID-19 (especially in China) along with better shipping situations, which could reduce inflationary pressures to some extent. However, uncertainties regarding Russia-Ukraine will likely be intact to weigh on oil prices which remains a key swing factor for overall macro economy,” Park of JP Morgan said.

“Although Kospi is currently trading at trough multiple, we expect decelerating inflation in the second half onwards to be the biggest market driver. Also, we should continue to monitor the degree of economic growth deterioration in exchange of alleviating inflation,” Park said.

Last month, South Korea’s consumer prices, a major gauge of inflation, jumped 5.4 percent on-year, the sharpest rise in almost 14 years. It accelerated from a 4.8 percent gain the previous month.

(mkjung@heraldcorp.com)

http://www.koreaherald.com/common/newsprint.php?ud=20220629000592